99905银河官方网站金骋路副教授与其在爱尔兰大学都柏林商学院导师JohnCotter教授和ThomasConlon副教授的合作论文“Co-Skewness across Return Horizons”于国际金融学知名期刊、ABS 3星期刊、公司认定的外文1级A期刊Journalof Financial Econometrics在线发表。

Abstract

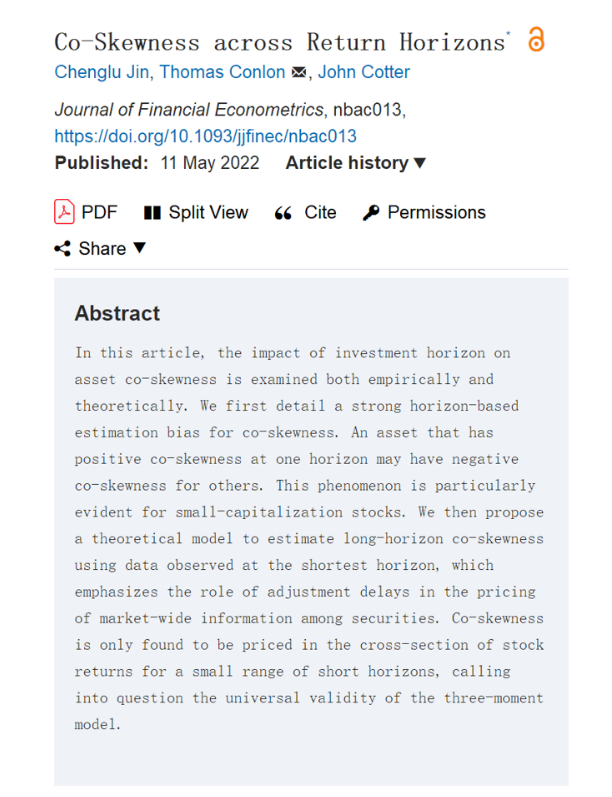

In this article, the impact of investment horizon on asset co-skewness is examinedboth empirically and theoretically. We first detail a strong horizon-based estimationbias for co-skewness. An asset that has positive co-skewness at one horizon mayhave negative co-skewness for others. This phenomenon is particularly evident forsmall-capitalization stocks. We then propose a theoretical model to estimate long-horizonco-skewness using data observed at the shortest horizon, which emphasizesthe role of adjustment delays in the pricing of market-wide information amongsecurities. Co-skewness is only found to be priced in the cross-section of stockreturns for a small range of short horizons, calling into question the universal validityof the three-moment model. (JEL G10, G12, G14)

摘要

本文从实证和理论上研究了投资期限对资产协偏度的影响。我们首先揭示了协偏度在不同投资期限间的估计偏误,即在一个期限下具有正协偏的资产可能在其他测度期限中具有负协偏,且这一现象对于小市值股尤为明显。然后,我们提出了一个理论模型,旨在基于单位期限内数据来估计更长期限的协偏度,该模型强调了定价迟滞在对股市资产定价的显著影响。协偏度被发现仅在较短的投资期限下的股票收益横截面中被定价,这使基于三阶矩的资本资产定价模型的普遍有效性受到质疑。(JEL G10, G12, G14)

金骋路副教授,毕业于爱尔兰都柏林大学斯莫菲特商学院。主要研究兴趣为资产定价、金融科技、行为金融学。在国内外重要期刊如《经济研究》、《数量经济技术经济研究》、《International Review of Financial Analysis》、《Pacific-Basin Finance Journal》等发表多篇论文。该成果为其主持的国家自然科学基金青年基金项目《考虑期限特征的股票收益率高阶协矩建模与资产定价研究》的标志性成果。